WeChat コードをスキャンしてご連絡ください

WeChat コードをスキャンしてご連絡ください

お気軽にメールをお送りください。できるだけ早くご返信させていただきます.

心と魂で未来を創る

01 Basic Situation

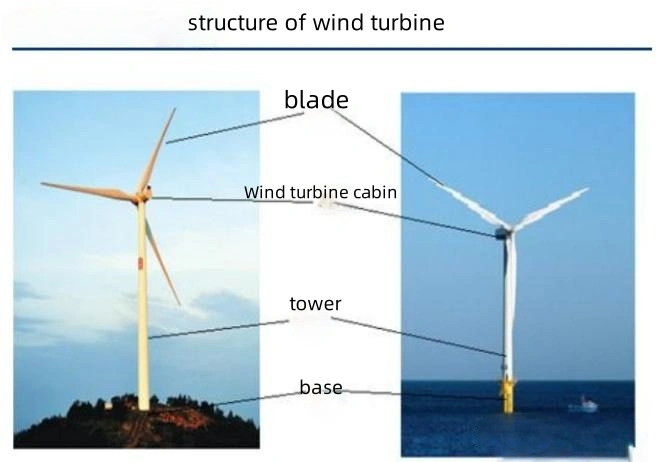

Wind power generation utilizes wind to drive the rotation of wind turbine blades and then increases the rotational speed through a speed-increasing machine to generate electricity with a generator. Compared to thermal power, wind power is more environmentally friendly; among clean energy sources, wind power technology is the most mature and has the lowest cost.

The wind power industry is a key strategic area for the development of clean energy. In the “14th Five-Year Plan”, China explicitly proposed to significantly increase the scale of wind power and orderly develop offshore wind power construction.

02 Industry Chain

の 風力発電 industry chain comprises upstream raw material enterprises and component manufacturers, midstream wind turbine manufacturers and tower suppliers, and downstream wind power operators. The upstream raw materials primarily refer to the raw materials used in wind turbine blade production, including resins, glass fibers, and core materials. Components mainly include blades, ギアボックス, generators, 塔, main shafts, and braking systems, とりわけ.

The core component of wind power is the generator set. The generator set includes the wind turbine, generator, and other components; the wind turbine is composed of blades, hubs, reinforcing parts, and other components. Blades and gearboxes are the components with the largest proportion and highest value in the cost structure of wind turbine units. Blades account for approximately 23% of the total unit cost. The size of wind turbine blades is increasing. According to analysis, increasing the blade diameter by 27.5% can reduce the cost per kilowatt-hour by 30%. The technical barriers for large blades are relatively high, requiring them to be both large and lightweight yet strong. 現在, the top five players account for approximately 70% of the market share. China Materials Technology has held the top position in the blade market for nine consecutive years, primarily supplying Goldwind Technology. The gearbox, located inside the nacelle, is currently the weakest link in the transmission chain of megawatt-level wind turbines. It is a component that is prone to overload and premature failure.

There are two technical routes: semi-direct drive and doubly fed induction generator, each with its advantages. Wind power bearings are the wind power structural components with the lowest degree of localization. High-end bearings for large-power models mainly rely on imports. Although domestic enterprises such as Luoyang Bearing, Wafangdian Bearing, and Xin Qianglian have achieved product shipments, their combined market share is less than 10%. Pitch and yaw bearings are primarily used to adjust the orientation of the wind turbine and the pitch angle of the blades, achieving a relatively high degree of localization. In the midstream of the industry chain, China has a strong competitive advantage in wind turbine manufacturing. Six of the top 10 global companies are Chinese, and none of the top 10 domestic companies are foreign-owned.

Goldwind Technology, Envision Energy, and Mingyang Smart Energy are the three leading players in the industry. Siemens Gamesa, Mitsubishi Vestas, Shanghai Electric, and Goldwind Technology dominate the global market share of offshore wind power. Wind turbine towers primarily use steel plates as raw materials, with the primary indicator being stability. The customer barrier is greater than the technical barrier. In China, the market is dominated by four companies: Tianshun Wind Energy, Taisheng Wind Energy, Dajin Heavy Industry, and Tianen Heavy Industry. These four companies have multiple production bases in coastal and three-north regions. The wind turbine control system is used to monitor the power grid, wind conditions, and operating parameters of the unit. It controls the grid connection and disconnection of the unit to ensure the safety and reliability of the operation process. 同時に, it also optimizes the unit’s control based on changes in wind speed and direction to improve the unit’s operating efficiency and power generation. The downstream of the industry chain is wind power operation. It has a high initial investment and a long project cycle, primarily dominated by large new energy power generation groups, mainly the “Five Major and Four Minor” groups. の “Five Major” are Huadian Group, Huaneng Group, Guodian Group, Datang Group, and State Power Investment Corporation. の “Four Minor” are China Resources Power, Guohua Power, State Investment Power, and China General Nuclear Power. Their combined market share is about 70%.

03 Industry Development

The Global 風力エネルギー Council predicts that by 2025, the global installed capacity of wind power (including both offshore and onshore wind power) will reach 73.4 GW, with an average annual compound growth rate of nearly 4%. The development of wind power is gradually shifting from onshore wind power to a dual development of both offshore and onshore wind power. The development trend of offshore wind power is towards deeper waters and farther seas. Leading enterprises with core technologies have a distinct first-mover advantage. 現在, the industry concentration is relatively high, with the top three players accounting for nearly 85% of the market share. Offshore wind farms are becoming larger in scale and more clustered. Through technological advancements, such as the development of larger wind turbines, the cost of offshore wind power is rapidly decreasing, and domestic offshore wind power is expected to enter a period of rapid growth.

サプライヤー

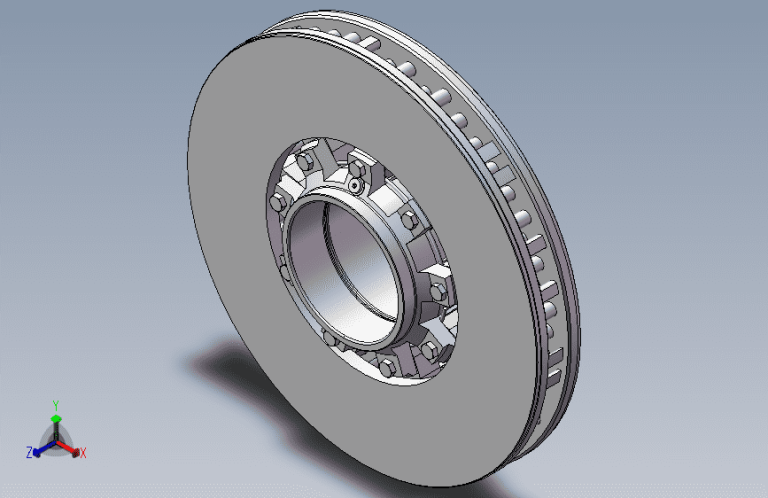

洛陽豊洋重工業株式会社, 株式会社, 1998年に設立された鉄道鋳造部品のメーカーです. 当社の工場面積は72,600㎡です。, 以上の 300 従業員, 32 技術者, 含む 5 シニアエンジニア, 11 アシスタントエンジニア, そして 16 技術者. 弊社の生産能力は 30,000 年間トン. 現在, 私たちは主に鋳物を生産しています, 機械加工, 機関車の組立て, 鉄道車両, 高速鉄道, 鉱山機械, 風力, 等. 当社の製品はロシアに輸出されています, 米国, ドイツ, アルゼンチン, 日本, フランス, 南アフリカ,イタリアとその他の国.

接触: キャシー

電子メール:[email protected]

携帯:008615515321683